In Part I of How Do You Know It’s a Good Idea?, we saw that successful startups do not just focus on perfecting the product or technology – it is more important to understand the relevant market and customer needs in order to get to product and market fit. In this second installment, we will expound on the importance of understanding your competition and ecosystem fully to build a viable business model.

Design thinking methodologies teach us to take a human-centered approach to product design, ideating and iterating until we arrive at a final rendition that meets customer needs at a fair price. However, successful startups never look at their products or customers in isolation, but take care to put them in the context of the wider industry and contingent businesses within it. In particular, it is vital to thoroughly assess the ecosystem so as to understand who along the industry chain has the most control and how they can leverage that control against you. Similarly, when it comes to the competitive landscape, it is not enough to get a threshold level of understanding. Startups need to probe deep and make accurate assessments on a comprehensive set of metrics, including competitor concentration and structure, behavior and industry best practices.

Here are some techniques for assessing industry dynamics:

- Market entry strategies

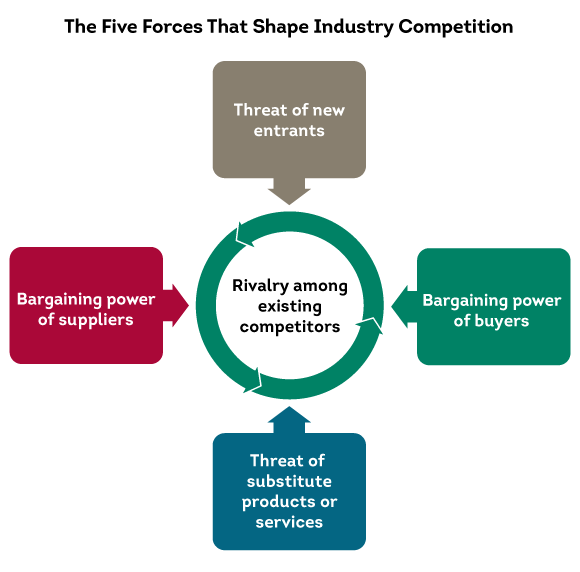

- Porter’s 5 Forces

- Industry Chain Analysis

We saw in Part I that the best technology doesn’t always win. Incorporating these ideas and keeping the big picture in mind, we can offer additional reasons as to why this might be true:

- Difficulty in obtaining access to the optimal distribution channels;

- Inhibitive costs (e.g, marketing, product, distribution);

- Difficulty in educating potential customers;

- Better connected competitors;

- Your tech isn’t vastly better than alternatives: 10x better is the benchmark to ensure switching

- 10x faster

- 10x cheaper

- 10x more usable

- 10x more efficient

To put these points in context, we share the story of TiVo, a promising technology that had every reason to take off, if not for the vital mistakes it made.

TiVo was invented in the 1990’s by Jim Barton and Mike Ramsay, the pioneers of digital device recorder (DVR). The device records TV content onto a hard disk and makes it available on-demand, without requiring a tape as VCR did. Jim and Mike also incorporated advanced features such as recording set based on series, actors, or interests, skipping commercials and rewinding live TV. All these developments were unprecedented at the turn of the millennium. In hindsight, TiVo was creating a new market, a market that we know for a fact would take off in the decades that follow. Indeed, at the time of launch, Forrester predicted that the company would reach 50% household penetration in 5 years. Fast forward today, streaming and on-demand content is ubiquitous, but the household name isn’t TiVo. What happened?

I. “Why Do We Need TiVo?”

The first mistake Jim and Mike made was a lack of effort in building need awareness when carving out a new market. For a considerable period of time after launch, individuals were still unclear about what the product was and why they needed it. Consumers at that time were satisfied with watching TV on a set schedule, and were not actively seeking alternatives to improve that experience. Hence, there was significant inertia against making the switch.

TiVo’s marketing, on the other hand, focused on the wrong problem. Jim and Mike expected the consumers to understand the need and instead invested heavily in building a brand without concretely delineating the problem the device was designed to solve. The founders failed to recognize that in creating a new market, it is necessary to build need awareness before brand awareness. If the need is salient enough, and the product is decent, the brand will build on itself through word-of-mouth. But in TiVo’s case, despite great success with brand awareness – people adopted TiVo as a verb, putting it in the league of Google and Kleenex – and offering a beautiful solution, consumers did not have an incentive to buy in the absence of a clear need.

II. Lack of Appreciation of the Industry Structure

TiVo’s go-to-market strategy was straightforward – in order to get the device at home, consumers would have to actively go to a store to buy it. This created relatively high barriers for purchase, adding to the switching cost. However, if we take higher level view of the ecosystem that TiVo operated in, there was one clear ally that it could have established partnerships with to allow easy distribution: the cable providers.

The nature of the cable service provider industry was such that players had an interest in lowering cost of entry and monetizing on subscription. In this sense, placing advanced technology with heavy marketing such as a TiVo console was perfectly aligned with the providers’ strategy. Missing this essential piece of understanding, TiVo failed to leverage this synergy and essentially turned an important ally into competitor. As a result, TiVo struggled from lack of distribution.

Later entrants who were able to recognize this opportunity capitalized on the relationship by offering DVR that came bundled with the cable service. It then became vastly easier to sign on consumers when the service is provided as an add-on to cable, lowering switching cost.

TiVo’s case study offers important insights into bringing to market an innovation. In particular, startups should have an accurate understanding of the existing product, consumer relationship with that product, and the best way to establish your innovation as the ultimate solution. It is also crucial to keep in mind that within an ecosystem, different pieces can work together to mutual benefits. When considering a go-to-market strategy, think big and think ecosystem.